recent development and outlook: high debt is of concern, April 2018

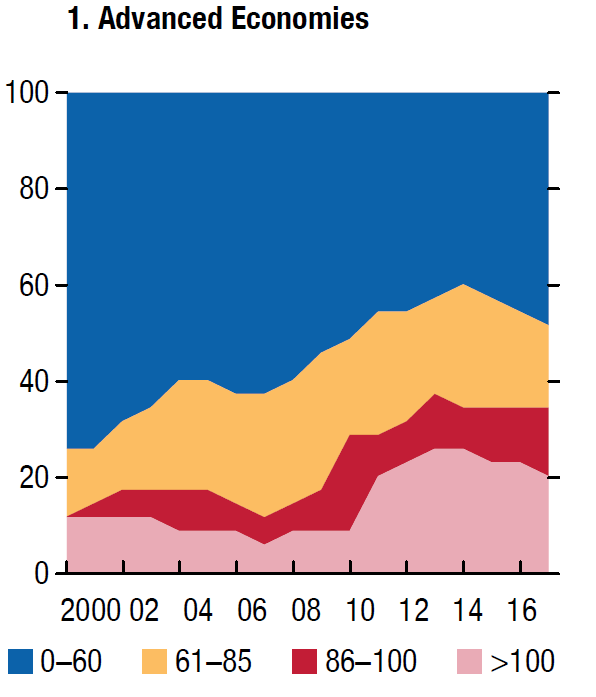

A large number of countries have debt-to-GDP ratios above critical levels

Note: The IMF’s Debt Sustainability Analysis for Market Access Countries identifies the critical debt thresholds—beyond which debt sustainability is put at high risk—as 85 percent of GDP for advanced economies and 70 percent of GDP for emerging market economies. The Joint World Bank–IMF Debt Sustainability Framework for Low-Income Countries finds critical thresholds to be 49, 62, and 75 percent of GDP depending on the country’s

institutional quality.

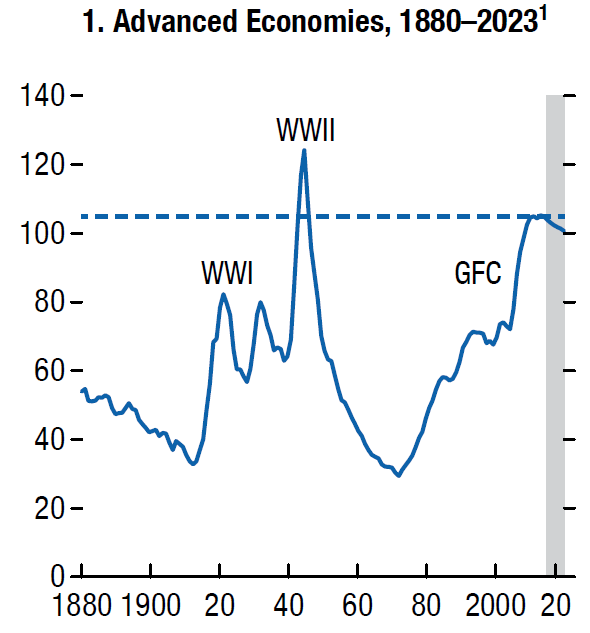

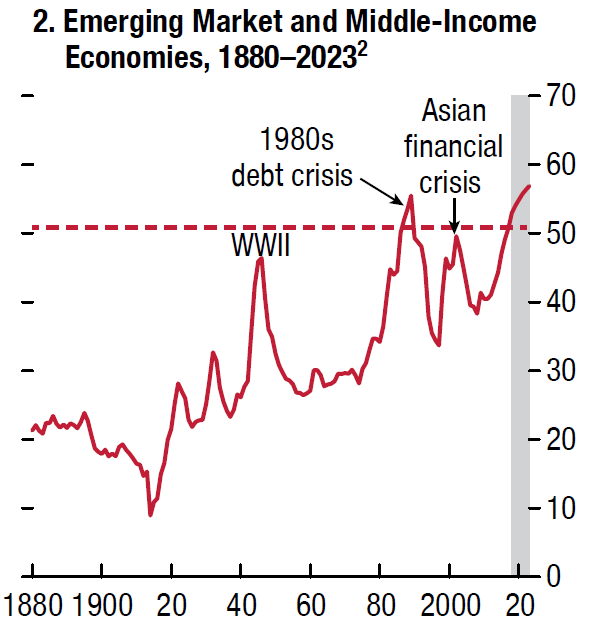

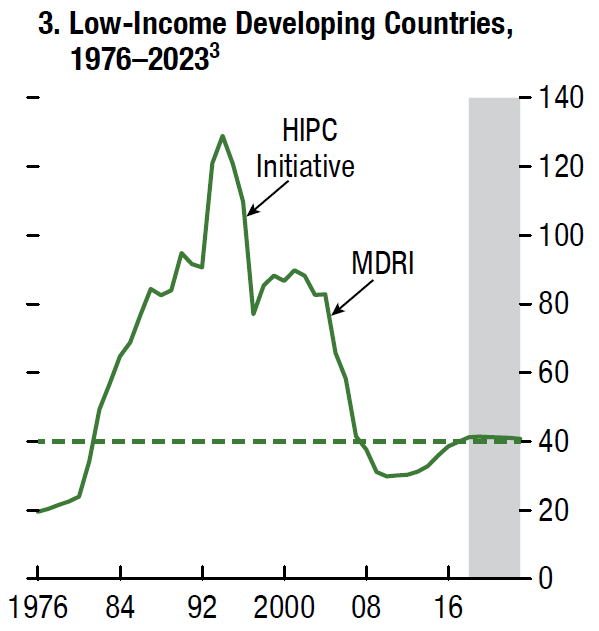

General Government Debt: Average debt-to-GDP ratios are at historic highs

Global debt is at historic highs, reaching the record peak of US$164 trillion in 2016, equivalent to 225 percent of global GDP. The world is now 12 percent of GDP deeper in debt than the previous peak in 2009, with China as a driving force.

Public debt plays an important role in the surge in global debt, with little improvement expected over the medium term. The rise in government debt reflects the economic collapse during the global financial crisis and the policy response, as well as the effects of the 2014 fall in commodity prices and rapid spending growth in the case of emerging market and low-income developing countries.

For advanced economies, debt-to-GDP ratios have plateaued since 2012 above 105 percent of GDP—levels not seen since World War II—and are expected to fall only marginally over the medium term. In emerging market and middle-income economies, debt-to-GDP ratios in 2017 reached almost 50 percent—a level seen only during the 1980s’ debt crisis—and are expected to continue on an upward trend.

For low-income developing countries, average debt-to-GDP ratios exceeded 40 percent in 2017, climbing by more than 10 percentage points since 2012, and are not expected to decline much over the medium term. Although the current level is below historical peaks for these countries, debt reduction from earlier peaks was driven by debt forgiveness and restructuring.

Underpinning debt dynamics are large primary deficits, which are at their highest in decades in the case of emerging market and developing economies. In the case of advanced economies, there has been little improvement in primary balances since 2015. Full Report

Debt-to-GDP ratios more than double when implicit liabilities linked to aging are included

General Government Debt Including Implicit Liabilities from Pension and Health Care Spending, 2017 (Percent of GDP)

SAVING FOR A RAINY DAY

With near-term growth on stronger footing, policymakers can turn their attention to rebuilding buffers and supporting medium-term growth. The pickup in economic activity in 2017 has been broad-based and continues to strengthen in 2018, suggesting that fiscal stimulus to support demand is no longer the priority. Rather, focus should now be on a twofold strategy to support growth over the medium term.

First, countries need to build fiscal buffers now by reducing government deficits and putting debt on a steady downward path. This will create room for fiscal support in case of a downturn and prevent fiscal vulnerabilities from becoming a source of stress on the economy if financing conditions tighten suddenly.

Second, such a fiscal adjustment needs to be anchored on structural fiscal reforms that support potential growth by promoting human and physical capital, and by increasing productivity. Full Report

All photography by Jared Chambers