Crypto Assets: New Coin on the Block, Reach for Yield, or Asset Price Bubble? APRIL 2018

Price Appreciation: Comparison with historical bubbles

Amid stretched valuations in many risky asset classes, crypto assets have erupted onto the financial landscape and their prices have skyrocketed. Some of the technological advances behind them have the potential to increase the efficiency of payment systems and the financial infrastructure. There has been a notable proliferation of crypto assets in recent years and major US exchanges have launched futures contracts.

However, crypto assets have also been afflicted by notorious cases of fraud, security breaches, and operational failures and have been associated with illicit activities.

At present, crypto assets do not appear to pose macrocritical financial stability risks. Policymakers, however, will need to be nimble, innovative, and cooperative to tackle potential financial stability challenges should crypto assets be used more widely. Full Report

Size: Crypto assets account for a small fraction of G4 central bank balance sheets

Bitcoin’s realized volatility is much higher than that of other asset classes

Risk-adjusted returns of crypto assets have not dramatically exceeded those of other mainstream assets

Sources: Bloomberg Finance L.P.; CoinDance; CoinMetrics; European Central Bank; Haver Analytics; national central banks; Yale International Center for Finance; and IMF staff estimates. Note: Panel 3 is based on 90-day realized volatility. In panel 4, crypto assets is an average across Bitcoin, Ethereum, Litecoin, and Ripple. The Sharpe ratio is the average return earned in excess of the risk-free rate per unit of total risk. EM = emerging market; FANGs = equal-weighted index of highly traded stocks of technology and tech-enabled companies such as Facebook, Amazon, Netflix, and Alphabet’s Google; FX = foreign exchange; G4 = Group of Four (Euro Area, Japan, United Kingdom, United States); TOPIX = Tokyo Stock Price Index.

Correlation of Bitcoin with Key Asset Classes and within Crypto Assets

Sources: Bloomberg L.P.; and IMF staff estimates

Note: Correlations are calculated over September 2015–March 2018. ETF = exchange-traded fund.

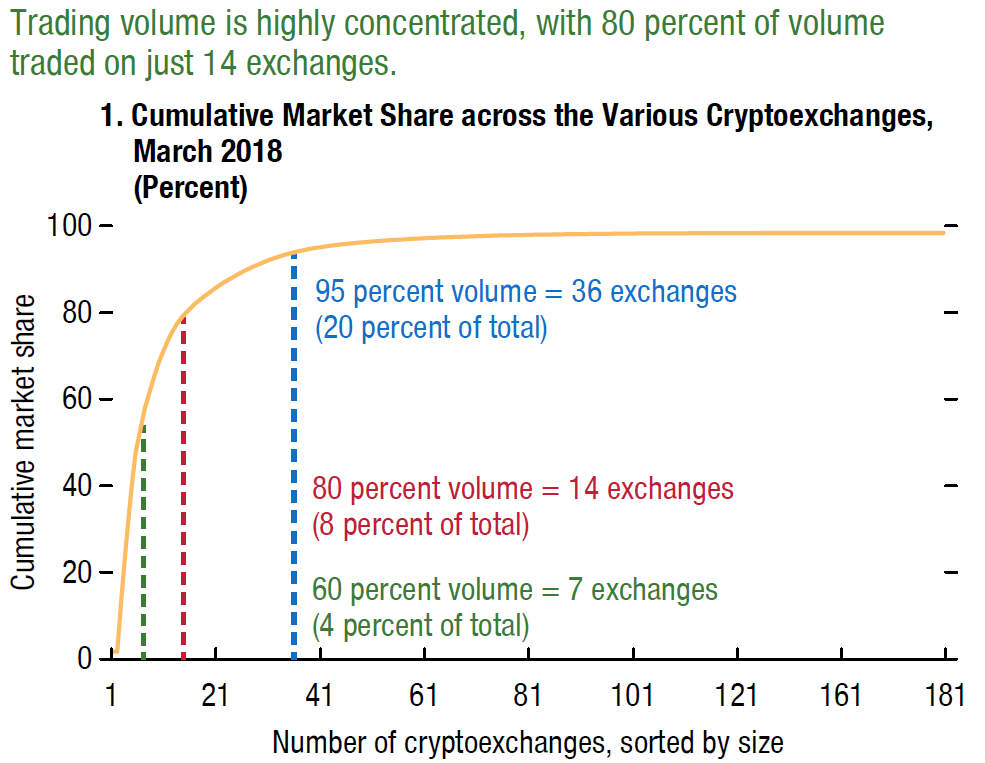

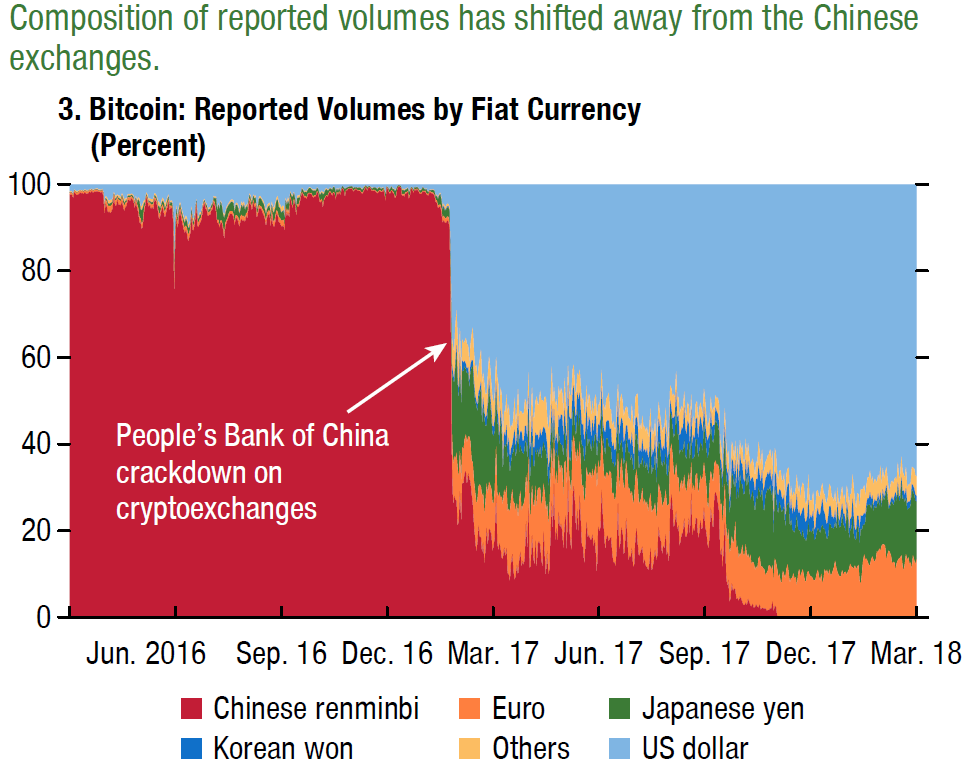

Share of Trading Volumes across Exchanges, Crypto Assets, and Fiat Currencies

Crypto Assets: A New Asset Class and Means of Payment?

Crypto assets have the potential to combine the benefits of traditional currencies and commodities. Like fiat money, they can potentially be exchanged for other currencies, be used for payments, and store value.

As investment products, they may offer portfolio diversification, although their ability to do so is still limited by their short track record, regulatory uncertainty, and primitive market infrastructure.

The technology underlying crypto assets—distributed ledger technology (DLT)—could also lead to more efficient market infrastructure. This technology differs from traditional payment systems, which require a clearing entity, such as a central bank, that settles transactions and distributes funds between participants.

DLT, in contrast, uses multiple copies of the central ledger, which are kept by individual entities. Blocks of transactions are subsequently validated and recorded, forming a historical chain—hence the name blockchain.

New units of the major crypto assets are supplied by “miners” who solve a cryptographic puzzle as part of the validation process and receive a new coin in return.

This procedure, however, is costly in terms of both energy and time. The supply process differs somewhat across crypto assets and allows for some flexibility. For example, there is an upper limit on the eventual outstanding amount of Bitcoins. But crypto assets can be designed without such an upper limit, thus mimicking more closely the money supply dynamics in traditional fiat money systems.

Crypto assets have been touted as a new form of money. However, they are still far from fulfilling the three basic functions of money. While they may serve as a store of value, their use as a medium of exchange has been limited, and their elevated volatility has prevented them from becoming a reliable unit of account.

These shortcomings could change with wider adoption and technological improvements, and some crypto assets may be able to perform the functions of money better, thus putting competitive pressure on fiat currencies.

Even after accounting for recent price corrections, crypto assets have experienced spectacular appreciation over the past year, spurred by the global reach for yield.

Nonetheless, they represent only a small share of the global financial system. Their total market value is less than 3 percent of the combined G4 central bank balance sheets.

Bitcoin alone accounts for 47 percent of crypto assets’ market value, while the next two largest crypto assets, Ethereum and Ripple, account for 15 percent and 8 percent, respectively.

As such, crypto assets currently pose limited challenges to fiat currencies or to the conduct of monetary policy. The dramatic growth in the sector, however, may pose risks to financial stability in the future and thus warrants vigilance by regulators.

Much attention has been devoted to the skyrocketing prices of crypto assets in 2017, which has invited comparisons with past speculative bubbles.

However, after accounting for price volatility, risk-adjusted returns have not dramatically exceeded those of mainstream assets over the medium term, though they have in the most recent year.

For example, the Sharpe ratio of crypto assets was relatively close to the risk-reward ratio of the S&P 500 over the past three years, and it was below what investing in so-called FANG stocks (Facebook, Amazon, Netflix, Google) would yield.

However, crypto assets have not been correlated with other assets, and therefore could provide diversification benefits to investors, on balance. The unconditional correlation between Bitcoin and other asset classes was close to zero between September 2015 and March 2018.

Even during the most recent bout of volatility, the correlation of Bitcoin with most mainstream assets did not appear to change significantly.

Pairwise correlations between different crypto assets are comparatively subdued, again despite tremendous variance in returns. Although these correlations are positive, they are somewhat lower than correlations with G4

sovereign yields and equities.

However, it is important to note that these correlations may change over time. So while some investors are beginning to investigate whether crypto assets could be an asset class in their own right, it is too early to draw clear conclusions. Full Report

All photography by Jared Chambers